The Best Personal Finance Book for Your Personality

This post may contain affiliate links. If you purchase a product through one of them, we will receive a commission at no additional cost to you. As Amazon Associates, we earn from qualifying purchases.

Today we are talking about the best personal finance book for your personality.

Yep, book.

Call me old fashioned, but I truly believe if we all read books as often as we read Instagram captions, then the world would be a happier place. I admit that I spent much of my 20s avoiding books altogether. It wasn’t until a re-watch of the classic film Good Will Hunting that I felt the sting of Matt Damon’s line:

“You wasted $150,000 on an education you coulda got for $1.50 in late fees at the public library.”

Oof.

Yes, I could have traded those expensive, hoity-toity college discussions on The Complete Works of Plato with Professor Steenson on the quad for a few committed hours of reading and a night at the bar.

I found myself convicted by this statement around the year 2014 and re-committed myself to reading about the things I wanted to understand. Interior design? I discovered a lovely book that explained the ins and outs of choosing paint colors. Gluten free cooking? (My jam for the last decade). I found a few cookbooks that addressed the issue. Personal finance?

Ah. Personal finance.

That, my friends, is likely a topic that was not available for coursework while obtaining your bachelor’s degree.

Fear not. I’m here for you. Once I read one personal finance book, I read another… and another… and another…

By this point, my library checkout history boasts just about every personal finance book available. I became addicted to them – dissecting the ins and outs of various gurus’ opinions and making them work for me.

In this post, I’m going to recommend 5 literary pillars of personal finance based on personalities.

Before We Begin…

Pause – let’s nip a couple of things in the bud before we begin, shall we? These are the excuses I used to tell myself about personal finance books.

Excuse #1: Why Read? I Don’t Have Time.

I’ve got news for you.

You don’t have time not to have time.

If you have time to watch Fuller House at 2am with a glass of three buck chuck, you have time to read for 15 minutes a day.

That’s all I’m asking for. 15 minutes a day. That’s literally 1% of your time. (24 hours times 60 minutes… divide 15/1440… move a decimal… yep! 1 percent.)

Why am I so adamant that it is imperative you get started, like, yesterday?

Because money needs time to grow. Compound interest working in your favor does not happen overnight. The earlier you start, the easier it will be.

Start now. Get your personal financial education going. You need time on your side.

You can do this.

Excuse #2: I’m Paying Off My Student Loans; I Can’t Afford Books.

If you live in America, you likely have a library at your disposal. In our town, our library is hooked up to a cooperative system – meaning we have access to all the books in all the libraries within a 40 mile radius.

Get yourself a library card and READ, dear friends.

Kindle lover? Most libraries nowadays have e-book downloads. You don’t even have to stress about returning them – they just disappear from your account when they are due.

Audio book lover with a long commute? You can download those from your library, too.

Besides, if you use the library, then you don’t have giant books sitting around your digs. The less books you purchase to keep, the less books you’ll have to pack up and move into your house when you buy it one day. 😉

The Best Personal Finance Book for Your Personality

Now that we have those pesky hindrances out of our way, let’s take a spin around the books I’d personally choose for a semester of Personal Finance 101.

I have these divided by personality type. Choose one or choose all, but do yourself a favor and commit to reading at least one by the end of the month.

Some of these books may contradict each other in the nitty gritty, but all have similar themes. Eventually you will have to decide what works best for you and form your own opinions. But in the meantime… just pick one and get started.

Without further ado, let’s jumpstart your personal finance health…

I Need Tough Love to Whip My Debt-Laden Ass Into Shape: The Total Money Makeover by Dave Ramsey

If debt is the hurdle between you and your dreams, Dave Ramsey is the guru for you. He is a straight shooter with a real plan, teaching 7 tried-and-true baby steps that work for real people with real lives. Any one of his books or plans will do, but a good place to start is The Total Money Makeover.

Dave Ramsey is known for unapologetically addressing people’s true issues underlying their money habits. Saunter over to his Youtube channel to get a taste of his very effective and direct way of communicating.

My favorite Dave Ramsey quote: “Debt is not a math problem, it’s a behavior problem.”

Not to mention – his community and even his Instagram feed are so inspiring, you’ll want to get started on paying down debt yesterday. It’s crucial if you want to jumpstart your personal finance health. Start today!

Nonfiction Is Boring and I’d Rather Read a Novel: The Richest Man in Babylon by George S. Clason

According to Wikipedia, which explains it better than I can:

“The Richest Man in Babylon is a 1926 book by George S. Clason that dispenses financial advice through a collection of parables set 4,000 years ago in ancient Babylon. The book remains in print almost a century after the parables were originally published and is regarded as a classic of personal financial advice.”

I can’t say I loved this book – not because of its content but because I really don’t have the patience for fiction. (I am the cold-hearted soul that couldn’t make it past the first chapter of Harry Potter.) However, just because I didn’t like it doesn’t mean you shouldn’t read it. If you best understand lessons via parables and stories, then this is the personal finance book for you. All the tenets of good financial habits are there – my favorites are saving 10% of your money, controlling your spending, and paying yourself first.

Like, I Totally Don’t Care About Finances or Whatever, but I Know They’re Super Important: Rich Bitch by Nicole Lapin

A wildly successful television host, Nicole Lapin reads like you’re out at brunch having mimosas with your besties. I love that her approach to personal finance is practical – she doesn’t want you to set a budget to take away your lattes, rather she wants you to set a budget so that you can have a latte if you want one.

Lapin lays down the law while being extremely relatable and speaking in terms that our generation can understand. She’s not some “financial coach” or “certified financial planner” trying to drum up business from you. She’s your cheerleader, complete with good fashion sense and a colorful Instagram feed.

I personally disagree with her viewpoint regarding renting instead of owning, which contradicts the “real estate = wealth advice” from those mentioned here like David Bach and Robert Kiyosaki. But let’s remember, you must develop your own opinion to eventually take or leave the advice that works for you. For me, Rich Bitch provides overall great advice through a delightful read.

Talk to Me Like a Ted Talk: The Automatic Millionaire by David Bach

You may have heard of David Bach before, likely due to his widely known phrase, “the latte factor.” He has a slew of popular books out, from The Automatic Millionaire to Smart Women Finish Rich.

We began with The Automatic Millionaire Homeowner during our house search. Two specific passages changed our lives. One was his simple exercise of writing down, with dates and signatures, our goal for real estate. We accomplished our goal within two months of its deadline. Insane.

Secondly, Bach tells a story about an average couple who owned their house for many years, moved out, bought a second, kept the first one as a rental, did it one more time, and retired multi-millionaires. With examples like this, he makes the jumpstart of personal finance health possible for the normal person. He also writes in plain English, which is quite refreshing when you are just starting out with personal finance.

As for the Automatic Millionaire books – which, if you read enough of them, become repetitive – I like their concepts, but they don’t work for me personally. Why, you ask?

Well, I’m a freelancer. Maybe you are, too – many of us millennials work side jobs to make things happen. As a model who works regularly, I should have 15-20 different employers. It’s the nature of the business and a double-edged sword. I love Bach’s suggestion to make your savings contributions automatic, but as a freelancer, that’s not how it works. I don’t have a sparkly HR department with a direct deposit form to route money to my Roth IRA. Conversely, I am the HR department, and must remain disciplined to do this myself. Yes, with at least 10% of my check. Every damn time.

All that aside… David Bach knows what he is talking about. Read his stuff!

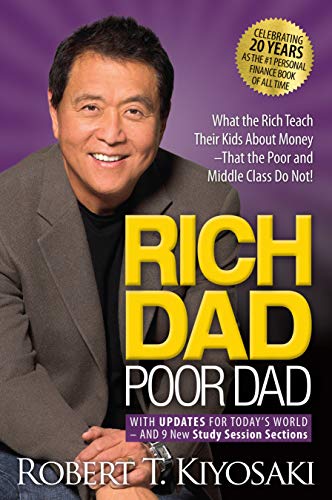

I Have No Feelings and Don’t Care if I Offend People: Rich Dad, Poor Dad by Robert Kiyosaki

A word of warning.

Rich Dad, Poor Dad by Robert Kiyosaki might make you very, very angry.

In this book, Kiyosaki describes the differences between his own dad, a college professor, and his friend’s dad, a business investor. I was shocked to learn that the college professor was the “poor dad.”

WHAT?!

Yes.

Kiyosaki may draw out a number of feelings from you. You might even go through stages of grief because, according to this book, your good grades, college education, and 9-5 job won’t necessarily jumpstart your personal finance health.

The main takeaway for us: acquire assets to work for you. An investment property like a 2nd unit or an Airbnb works for you. Renting your car on Turo turns a depreciating asset into something that works for you.

I will admit, Kiyosaki pushes my buttons, and he’s not my favorite finance guy. However, I credit his book for the huge mental shift that brought me to the investor mindset.

About that – investor mindset – there is a reason I have listed this book last on this list. It’s because you must have your personal finances straightened out before you advance to asset acquisition. If you’re not practicing good habits with a checking account balance of $300, then you have no business buying a property worth $300,000. So, before you get excited to purchase a bunch of assets, please, sort out your personal finances – particularly with debt – and then move on to the “advanced class” of investing with Robert Kiyosaki.

Conclusion

There you have it, my friends. Our first semester’s reading list on Personal Finance 101. We can catapult ourselves in the direction of success and expedite the trip with a little help from these wise ones.

Don’t forget to subscribe to Our Two Family to never miss a post!