The Popular Brrrr Method + 8 Boring Reasons We Ditched It

This post may contain affiliate links. If you purchase a product through one of them, we will receive a commission at no additional cost to you. As Amazon Associates, we earn from qualifying purchases.

Today at Our Two Family house, we are breaking down the BRRRR Method of real estate, plus the reasons Derek and I decided not to follow through with the whole process.

Many people love real estate for its capacity to leverage – and indeed, we have reaped the benefits of leverage from our house purchase.

But there were some things with an aggressive BRRRR that didn’t sit right with us, and we will be sharing those reasons below.

But before we get to that… what’s the BRRRR method?

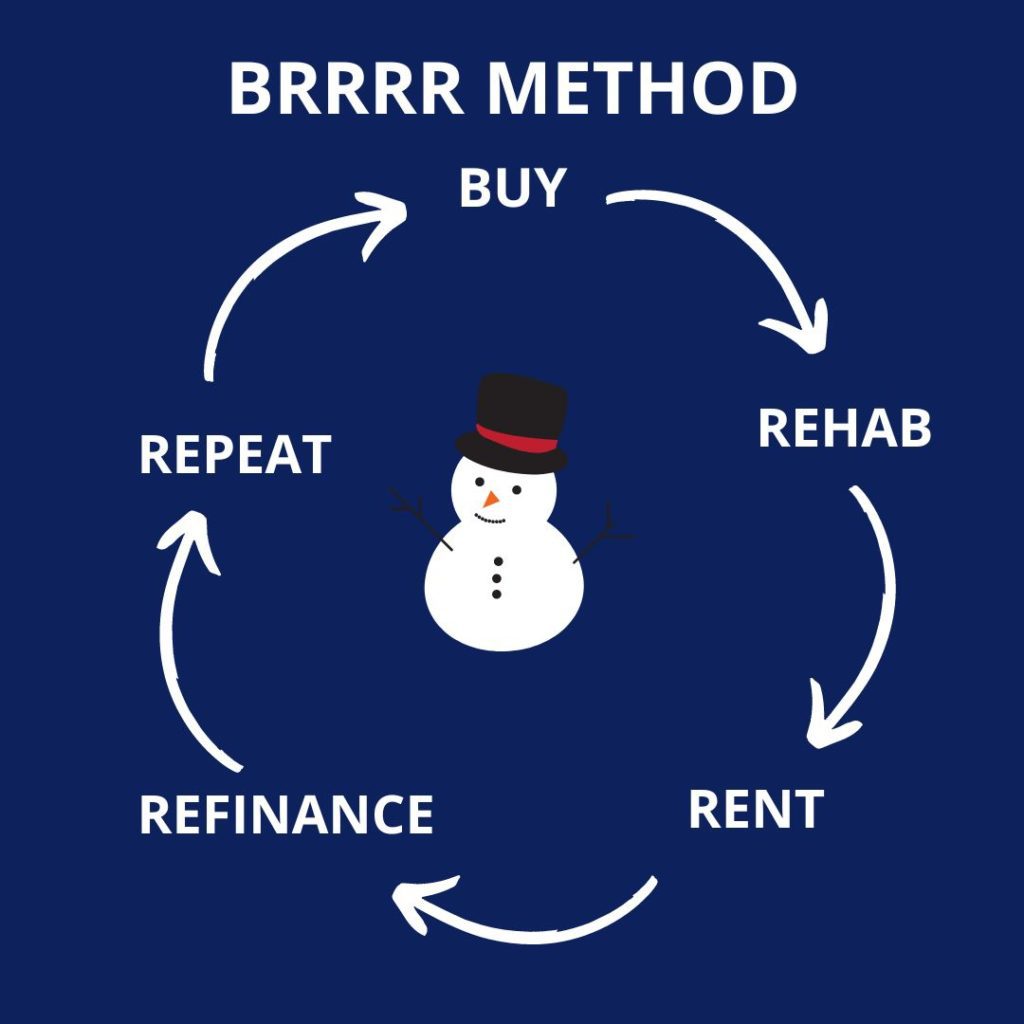

What’s the Brrrr Method?

The BRRRR method is a real estate investing acronym coined by Bigger Pockets. BRRRR stands for:

- Buy

- Rehab

- Rent

- Refinance

- Repeat

The basics are as follows:

- Buy – you buy a property

- Rehab – you fix the property

- Rent – you rent out the property to tenants

- Refinance – you refinance the property – typically taking out the cash you’ve made from the rehab

- Repeat – buy another property with the cash from your refinance.

A successful BRRRR depends on many factors – including buying the house a low price, rehabbing it enough that you’ll make enough money on your after-repair value (ARV) to refinance, and oh yes – your tenants actually paying on time to cover your mortgage.

When we first bought our two family house, we knew that there was ample room for significant improvement via rehab. We also knew that with a good tenant, our location would yield high rent. However, we did not commit to a full BRRRR.

Here are the reasons – though we completed the buy, rehab, rent, and refinance – why we did not repeat this process.

Brrrr Method Example

Let’s look at a basic hypothetical example to explain.

You buy a house at $100,000. With a down payment of 20%, or $20,000, you take out an $80,000 mortgage.

You fix the house (rehab). It costs you $30,000 for all the rehab. Out of pocket so far, you’re at $50,000.

You rent out the house. (We’ll assume your tenants pay on time, yay!)

You refinance the house. Here’s the fun part: its after repair value is now $150,000.

Pretty good.

Now, if you want to, you can leave 20% of the house value in the home, and take out the rest of your money.

Think of it like buying the house all over again. It’s a $150,000 house, so you would put $30,000 down. You’ll take out a $120,000 mortgage. You now get your initial investment of $20,000 back out of the house. If you’ve done your math right, your tenant’s rental payment should cover this newer, bigger mortgage.

And, if you want to, you can repeat the entire process with that $20,000 and buy another house.

Reasons We Didn’t Brrrr

As the title of this post states, we did not fully complete a BRRRR cycle.

We bought, we rehabbed, we rented, we refinanced, but we did not repeat.

Here are the 8 reasons why.

1. High Market

We bought our house in fall of 2016.

Little did we know, we bought just before the “curve” was headed sharply north. This has worked in our favor because the value of our property – and our rental – have done nothing but go up, fast. (Yes, real estate in general goes up most years, but the past 6 years have been exceptional in growth, no?).

If we were going to “repeat” using the BRRRR method, we’d need to find a property (a) that we could afford and (b) that was cheap enough that the after-repair-value would be worth it.

We tried, we really did. But every time we looked at another property, we passed. Check out our post, 10 Reasons Not to Buy a House for all the wild stories on what we didn’t buy!

No matter what, BRRRR or not, buying a property too high will always kill a deal. Mostly due to high prices, we just haven’t bought another yet.

2. Tenants Don’t Always Pay

One very significant assumption of the BRRRR method is that your tenant will pay.

Read that again.

The BRRRR method assumes that your tenant will pay.

I’ve got sad, sorry news.

Tenants don’t always pay. Even the good ones.

Something comes up. The bank transfer didn’t work. The paycheck doesn’t come until Friday, and the first of the month is Wednesday. They vacationed to Cancun and forgot all about their apartment at home.

Sometimes – not all the time, but sometimes – tenants are tenants because they are not responsible enough with their money to own a home.

If you are planning to BRRRR, choose your tenants very carefully. One of the biggest BRRRR method risks is a nonpaying tenant.

We have had two wonderful tenants so far. We have still dealt with delayed payments for one reason or another.

With these experiences, the thought of leveraging a second property and relying on the tenant’s payment to cover the mortgage every month was too risky for our taste.

Side note for the critics out there – yes, we do keep a cash reserve for our property, which has mortgage payments built in for extreme situations such as a nonpaying tenant. We would do the same for a second property. Nevertheless, we remain risk-averse when it comes to tenant payments.

You might be less risk-averse and totally comfortable with the idea that your tenant will pay up each month and your mortgage will be fine.

Good for you! Seriously. If that’s your jam, go after it.

3. We Weren’t Desperate for Cash

One of the benefits of the BRRRR method is that you get cash out of your house.

In our example above, you would get all of your $20k initial capital out of the deal.

While we did refinance (more on that below), we did not take cash out. Why?

Accessing capital wasn’t our problem! (Crumbling exterior stair with ugly curb appeal – more like our problem).

We still had enough money saved up for our near-future renovations. As DINKs – double income no kids – we were both working, keeping our personal costs down, and saving up for renovations from our income. We surmised that, if we really liked another property and needed a down payment, we could always take out cash later.

Related: How to Budget for Buying a House

4. Private Mortgage Insurance

We wanted to get out of PMI, not into more of it. Sometimes, investors will BRRRR so hard that they’ll end up with more PMI.

Ah. Did anyone tell you about PMI?

PMI – private mortgage insurance – is an extra couple hundred bucks per month that the banks charge you to insure their butts in case your mortgage goes awry. It is tacked on to your mortgage payment when you put less than a 20% down.

It’s stupid. But you have to deal with it.

In some mortgages, you can eventually pay your way out of PMI. As in, once you reach the threshold amount of 20% down, you no longer pay PMI. If you bought a $100,000 house, once you paid down $20k on your mortgage and only had $80k left, then POOF! – no more PMI.

We used an FHA 203k Loan to purchase our two family home, with a down payment of 3.5%. Unfortunately for us at the time, there was no paying your way out of PMI on FHA Loans. As in, we would be stuck with that extra $212 per month, every month, until our mortgage was paid off in the year 2046.

NO THANKS!

So, after we finished our second floor renovation, we refinanced, confident that the full gut renovation would yield a good enough return to refinance into a conventional loan.

We were right! Our loan-to-value ratio squeaked in at 80% – right where we wanted to be. That means we now owned 20%, and mortgaged only 80%.

No more PMI.

5. Our Mortgage Would Go Up.

We also didn’t fully BRRRR because our monthly mortgage costs would go up.

Look at the example from earlier. The first mortgage was on $80,000. Assuming a 4% rate on a 30 year fixed mortgage with property taxes annually at $5k, the monthly payment would be around $870.

The second mortgage in our example above would be on $120,000. Assuming the same 4% rate on a 30 year fixed mortgage with property taxes annually at $5k, the monthly payment would be almost $1,100 per month.

Sure, $230 per month isn’t too big a deal. But that extra bit adds up quickly when you have more to renovate and a future to save for.

6. We Had Too Much to Renovate

We had so much more to renovate within our four walls, we didn’t feel ready to buy another property. So, we left the cash / sweat equity in the house.

One of the ways to make a BRRRR most profitable is to buy a property in bad condition.

If we had taken cash out of our home and bought another property – we’d also have to fix another property!

We just didn’t have the time or energy to devote to that. It wouldn’t have been impossible, but it just wasn’t for us.

We are very glad that we recognized that. Which brings me to my next point.

7. We’re Getting Rich Slowly, and We’re Ok With That

Something about the real estate game reminds me of high school gym class. There’s a palpable, yet futile, competition.

People like to toss out numbers – “15 doors in 3 years!” or, “From renter to 20 units in 6 months!” …as if more properties in shorter time means you are a real estate mogul success monster.

Stop.

Guys, let’s just stop.

If we’re all really in this to gain financial freedom, for the reasons of escaping the 9-5 grind or having more time with our kids – just stop it with the number comparisons.

Sure, you can boast about having 15 doors, but if each only brings in $50 profit per month, how far ahead will you really be? Or, if you own that 20 unit building but you’re drowning in a 95% leveraged building with tenants that don’t pay, is it really worth it?

My point is, don’t let catchy headline numbers sway your personal comfort level with leveraging real estate.

Could we have worked our little tails off and expanded to own more properties in the last 6 years? Sure. Yes, that would have been possible.

But we’re personally more at peace with our simple two family house for now.

8. There Is Such Thing as Over Leveraging.

Leverage is powerful. And, there’s such thing as too much of it!

We didn’t want too much personal liability. With the inconsistency of my freelance income paired with the unpredictability of tenants, we just weren’t comfortable with taking out a mortgage on a second property.

That doesn’t mean you can’t!

Take a moment and think about what kind of – and how much – leverage you are comfortable with. And if, at the end of the day, your name is on the mortgage, will you be able to keep your butt covered and the bank at bay (i.e. PAY IT) even if your tenant has a problem?

In hindsight, we are very glad we weren’t leveraged to the hilt for a couple of reasons:

- There happened to be a pandemic in 2020, along with an eviction moratorium, and in our state, we were relieved that we didn’t have umpteen mortgages to pay amidst tenants who legally faced no consequences for nonpayment.

- Mortgage rates can (and did!) turn upwards in a short amount of time this year (2022). Many investors got caught with their numbers messed up because they were relying on their refinance to have a lower interest rate. We were glad to have avoided this mess.

Is Brrrr Worth It?

We can’t say for sure if a complete BRRRR cycle is worth it.

We may have ditched the last step due to a high market, potential PMI, tenant inconsistency, mortgage costs, looming renovations, and the possibility of over leveraging. But, from our perspective, doing even the first 4 steps was definitely worth it!

Our comfort level puts us in our two family house for now, and that’s enough for our inner peace.

Related Posts:

- House Hacking a Duplex – Pros and Cons

- What Makes a Good Real Estate Investment?

- Is House Hacking Worth It?